Taking the first step toward recovery is an act of immense courage. The decision to seek help for a substance use disorder is a profound commitment to your health, your future, and the possibilities that life can offer when you are no longer defined by addiction. As you explore your options, you may find yourself looking beyond your local area, and even beyond national borders. The idea of traveling for treatment is becoming an increasingly popular and powerful choice for many individuals seeking a new beginning. This concept, sometimes called “medical tourism,” offers a unique set of therapeutic advantages. Removing…

Taking the first step toward recovery is an act of immense courage. The decision to seek help for a substance use disorder is a profound commitment to your health, your future, and the possibilities that life can offer when you are no longer defined by addiction. As you explore your options, you may find yourself looking beyond your local area, and even beyond national borders. The idea of traveling for treatment is becoming an increasingly popular and powerful choice for many individuals seeking a new beginning.

This concept, sometimes called “medical tourism,” offers a unique set of therapeutic advantages. Removing yourself entirely from the environment where addiction took hold can provide a true fresh start, creating physical and mental distance from the people, places, and routines that trigger substance use. This geographical separation allows you to disconnect from negative influences and enablers, giving you the space to focus solely on healing. Furthermore, seeking treatment abroad often provides a level of privacy and confidentiality that can be difficult to achieve in your home community, allowing you to engage in the recovery process without fear of judgment or social pressure. For some, it also opens the door to specialized treatment modalities or simply a higher quality of care that is more affordable than comparable options in the United States.

This path represents a significant emotional and financial investment in your well-being, a powerful declaration of your commitment to change. But it also raises a critical and practical question: Can your U.S. health insurance help pay for it?

For many, the answer is a hopeful “yes.” Using your domestic insurance for international rehab is often possible, but it requires understanding your rights, your specific policy, and a clear process. Navigating the world of health insurance can feel overwhelming, but it doesn’t have to be a barrier to getting the best care possible. This guide is designed to walk you through that process step by step, demystifying the jargon and providing you with an actionable roadmap to help you access a world of healing.

The Foundation of Coverage: Your Right to Treatment Under U.S. Law

Before diving into the specifics of international coverage, it’s essential to understand the legal foundation that makes it possible: The Paul Wellstone and Pete Domenici Mental Health Parity and Addiction Equity Act of 2008 (MHPAEA). This landmark federal law fundamentally changed the landscape of insurance coverage for mental health (MH) and substance use disorder (SUD) treatment in the United States.

The core principle of MHPAEA is “parity,” which simply means that health insurance plans are legally required to cover mental health and substance use disorders in a way that is no more restrictive than their coverage for medical and surgical benefits. This was a monumental shift. Prior to MHPAEA, insurers could place severe limitations on addiction treatment that they would never apply to conditions like diabetes or heart disease. The law ensures that if your plan provides a certain level of benefits for medical care, it must provide an equivalent level for addiction treatment.

In practical terms, this principle of parity applies across several key areas:

- Financial Requirements: Your plan cannot charge higher copayments, coinsurance, or deductibles for addiction treatment than it does for most medical or surgical services.

- Treatment Limitations: Insurers are prohibited from imposing stricter quantitative limits, such as the number of inpatient days or outpatient visits allowed per year, for MH/SUD care compared to medical care.

- Care Management: The criteria used to determine “medical necessity” and the requirements for getting pre-authorization for treatment must be comparable for both MH/SUD and medical/surgical benefits.

The Patient Protection and Affordable Care Act (ACA) later expanded on these protections by classifying mental health and substance use disorder services as one of ten “essential health benefits” that most individual and small group plans must cover.

This legal framework is the critical lever that opens the door for using U.S. insurance abroad. The law mandates that if a health plan offers benefits for out-of-network providers for medical or surgical care, it must also offer comparable out-of-network benefits for mental health and substance use disorder care. Since virtually all international treatment centers are considered “out-of-network” by U.S. insurance companies, the MHPAEA’s mandate is the fundamental reason why seeking coverage is a viable option. It transforms your inquiry from a request for a special exception into the exercising of a legally protected right under your existing health plan.

Decoding Your Policy: Why Your Plan Type (PPO vs. HMO) is the Key

Understanding your rights under federal law is the first step. The second, and equally crucial, step is understanding your specific insurance policy. In the U.S., health plans generally fall into two main categories: Health Maintenance Organization (HMO) plans and Preferred Provider Organization (PPO) plans. The type of plan you have is the single most important factor in determining whether you can use your insurance for international rehab.

HMO (Health Maintenance Organization) Plans

HMO plans are designed around a specific, local network of doctors, hospitals, and healthcare providers. To receive coverage, you are generally required to use only the providers within this network. These plans often require you to select a Primary Care Physician (PCP) who acts as a gatekeeper, meaning you need a referral from your PCP to see a specialist.

The critical limitation of an HMO plan is its lack of coverage for out-of-network care. With the exception of a true medical emergency, an HMO plan will typically not pay for any services received from a provider outside its contracted network. Since an international rehab facility is, by definition, an out-of-network provider, HMO plans are almost never a viable option for covering this type of elective, non-emergency treatment.

PPO (Preferred Provider Organization) Plans

PPO plans offer significantly more flexibility. Like HMOs, they have a “preferred” network of providers, and using them results in lower out-of-pocket costs. However, the defining feature of a PPO is that it provides benefits for out-of-network care. This means you have the freedom to see any doctor or go to any facility you choose, whether they are in-network or not, without needing a referral.

This out-of-network benefit is the primary mechanism that makes using your insurance for international rehab possible. When you attend an international facility with a PPO plan, your insurance will process the claims according to your out-of-network benefits. It’s important to understand that this coverage comes with a different cost structure. You will likely face:

- A Higher Deductible: You will have to pay more out-of-pocket before your insurance begins to contribute.

- Higher Coinsurance: Your plan will cover a smaller percentage of the cost. For example, it might cover 80% for in-network care but only 60% for out-of-network care, leaving you responsible for the remaining 40%.

- A Separate Out-of-Pocket Maximum: Many plans have a higher annual cap on what you have to pay for out-of-network services before the plan covers 100% of costs.

While other plan types like Point-of-Service (POS) may also offer some out-of-network coverage, PPO plans are the most common and straightforward vehicle for accessing international care. The table below provides a clear summary of the key differences.

| Feature | PPO (Preferred Provider Organization) | HMO (Health Maintenance Organization) |

| Provider Choice | Freedom to see any provider, in or out-of-network. | Must use providers within the plan’s local network. |

| Out-of-Network Coverage | Yes, but at a higher cost-sharing (higher deductible/coinsurance). | No coverage, except for true emergencies. |

| Referrals Needed? | Generally no referral needed to see specialists. | Usually requires a referral from a Primary Care Physician (PCP). |

| Viability for International Rehab | High. The out-of-network benefit is the primary pathway for coverage. | Very Low. Elective international care is typically not covered. |

Your Action Plan: A Step-by-Step Guide to Verifying Your Benefits

Once you’ve confirmed you have a PPO or similar plan with out-of-network benefits, the next step is to verify the specifics of your coverage. This process involves a direct conversation with your insurance provider. While it can seem daunting, being prepared with the right information and questions will empower you to get the clear answers you need. This verification is not just about confirming coverage; it’s a crucial financial forecasting tool that allows you to understand your potential total costs.

Step 1: Gather Your Tools

Before you make the call, have your insurance card in hand. Locate the following key pieces of information:

- Your Member ID Number

- Your Group Number (if applicable)

- The Member Services Phone Number, usually found on the back of the card.

Step 2: Make the Call and Ask the Right Questions

When you speak with an insurance representative, your goal is to build a complete picture of your financial responsibility. Use the following questions as a script to guide the conversation:

- “I am exploring options for residential substance use disorder treatment. Can you please confirm the details of my out-of-network benefits for this type of care?”

- “What is my current out-of-network deductible, and how much of it has been met for this year?”

- “After my out-of-network deductible is met, what is my coinsurance percentage for out-of-network inpatient or residential behavioral health services?”

- “What is my annual out-of-pocket maximum for out-of-network services?”

- “Is pre-authorization or prior certification required for out-of-network residential substance abuse treatment?”

- “Are there any specific coverage limitations, such as a maximum number of days, for this level of care?”

Each of these questions helps you calculate a realistic estimate of your total cost. The deductible is the initial amount you’ll pay. The coinsurance is the percentage you’ll pay on all costs after the deductible is met. The out-of-pocket maximum is the crucial “safety net” that caps your total spending for the year. Understanding these variables transforms a frightening, unknown expense into a predictable figure you can plan for.

Step 3: Document Everything

During the call, take meticulous notes. Write down the date and time of your call, the full name of the representative you spoke with, and be sure to ask for a reference number for the conversation. This documentation creates a crucial paper trail that can be invaluable if any discrepancies arise later.

Step 4: Let an Expert Help

Navigating this call can be stressful and confusing. The terminology is complex, and it’s easy to feel overwhelmed. This is why experienced international treatment centers have dedicated admissions teams who specialize in this process. Reputable centers, like Costa Rica Treatment Center, offer a complimentary insurance verification on your behalf. Their admissions navigators make these calls every day. They know the precise language to use and the right questions to ask to get a clear and accurate understanding of your benefits. This service removes the burden and confusion from your shoulders, allowing you to focus on what truly matters: your recovery.

The Critical Hurdle: Understanding Pre-Authorization

During your call with the insurance company, you likely heard the term “pre-authorization” (also called prior authorization or pre-certification). This is arguably the most critical step in the entire process, and failing to complete it can have severe financial consequences.

Pre-authorization is the formal process of getting approval from your insurance company before you are admitted for treatment. It is not simply a notification; it is a clinical review. The insurer requires this step to determine that the proposed treatment is “medically necessary” for your diagnosed condition. This is a standard gatekeeping procedure for most significant medical services, both in-network and out-of-network.

The process typically involves the treatment facility submitting detailed clinical documentation to the insurer. This may include your diagnosis, a proposed treatment plan, and notes from your referring physician that justify the need for residential-level care. The insurer’s clinical team reviews this information against their coverage criteria.

The importance of this step cannot be overstated. If your plan requires pre-authorization and you do not obtain it before beginning treatment, the insurance company has the right to deny the entire claim. This means you could be held responsible for 100% of the cost, even if the services would have been covered had you gotten approval beforehand.

Think of pre-authorization as the formal “handshake” between the international treatment center and your U.S. insurer. It is the point where your insurer officially acknowledges the proposed treatment and agrees, in principle, to cover it according to your plan’s terms. Receiving a formal approval letter or authorization number provides you with the assurance that your claim will be processed correctly. An experienced treatment center’s admissions team will manage this entire complex process for you, ensuring all necessary documentation is submitted and approval is secured before you travel.

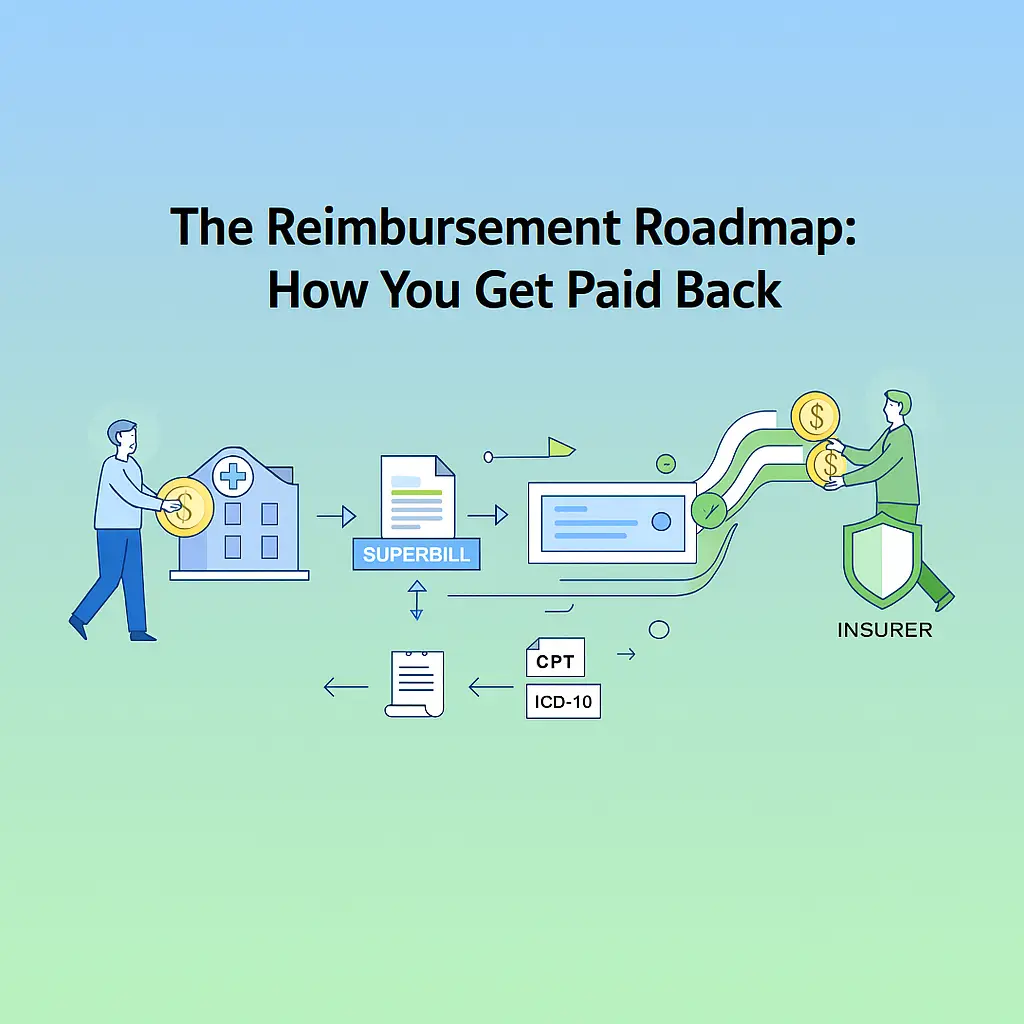

The Reimbursement Roadmap: How You Get Paid Back

Another key difference with out-of-network care is the flow of payment. Unlike in-network care where the facility bills the insurer directly, the process for out-of-network care is typically based on reimbursement. This means that you, the patient, will pay the treatment center directly for the services you receive. Afterward, you submit a claim to your insurance company, and they send a payment directly to you for the covered portion of the costs.

The key to this entire reimbursement process is a document called a superbill.

A superbill is a highly detailed, itemized receipt provided by the treatment center that contains all the specific information your insurance company needs to process your claim. A standard invoice is not sufficient; a superbill is a specialized document designed for the U.S. insurance system.

Essentially, the superbill acts as a translation document. It converts the holistic, therapeutic experience of rehab into the standardized, transactional language that U.S. insurance companies understand. An insurer in another country may not recognize terms like “equine therapy” or “mindfulness sessions,” but they do understand a universal system of medical codes. The superbill deconstructs your treatment into these billable, universally understood units.

To be accepted by an insurer, a superbill must include several essential components:

- Patient Information: Your full name, date of birth, and policy information.

- Provider Information: The treatment center’s legal name, address, National Provider Identifier (NPI), and Tax ID number (EIN).

- Diagnosis Codes (ICD-10): These are alphanumeric codes that represent your specific medical diagnosis, such as F10.20 for Alcohol Use Disorder, Severe. This justifies the medical necessity of the treatment.

- Procedure Codes (CPT): These are five-digit codes that correspond to each specific service rendered. For example, there are distinct codes for an initial psychiatric evaluation, a 45-minute individual therapy session, or a group therapy session.

- Dates and Costs: The superbill must clearly list the date each service was provided, the corresponding CPT code, and the fee for that service.

Once you receive the superbill from the treatment center (often on a monthly basis), you submit it to your insurance company’s claims department, typically through an online portal or by mail. The insurer then processes the claim and reimburses you according to your out-of-network benefits.

This highlights a critical, often overlooked factor when choosing an international rehab: their administrative experience with the U.S. insurance system. A center’s clinical excellence will be of little financial help if its billing department cannot produce a correct, U.S.-compliant superbill. A document with missing information or incorrect codes will be swiftly denied, delaying or preventing your reimbursement.

The Costa Rica Advantage: Where World-Class Care Meets Affordability

Now that you understand the mechanics of using your PPO plan for out-of-network care, you can begin to see how choosing an international destination like Costa Rica can be a strategic and intelligent financial decision. It allows you to leverage your insurance benefits to access a level of care and an environment that might be prohibitively expensive in the United States.

The primary benefits of traveling for rehab—a fresh start, enhanced privacy, and a singular focus on recovery—are amplified in a location renowned for its tranquility and natural beauty. The “Pura Vida” lifestyle of Costa Rica is not just a slogan; it’s an ethos that promotes peace, well-being, and a connection to nature, creating a uniquely therapeutic backdrop for healing.

Beyond the environment, there is a significant financial advantage. The cost of premier, residential addiction treatment in the U.S. can be staggering, with luxury facilities often charging $30,000 to $100,000 or more for a 30-day stay. In contrast, top-tier, accredited facilities in Costa Rica can offer equivalent or superior care—with high staff-to-client ratios and comprehensive, evidence-based therapies—for a fraction of that cost.

This cost difference has a direct and powerful impact on how your insurance benefits work for you. A lower total cost of treatment means your out-of-network benefits go much further. You will meet your deductible and your out-of-pocket maximum far more quickly, and your total financial responsibility (your coinsurance portion) will be significantly lower. This is a form of “healthcare arbitrage”—using your insurance plan strategically to maximize the value of your healthcare dollars. You can access a level of care, comfort, and personalized attention that might be financially out of reach at U.S. out-of-network prices.

Choosing a center like Costa Rica Treatment Center means you’re not just choosing a location; you’re choosing a partner that combines this serene, therapeutic environment with the administrative expertise to help you navigate your U.S. insurance benefits effectively. We understand the requirements of U.S. insurers and are experienced in providing comprehensive, compliant superbills to facilitate your reimbursement. Our team is dedicated to making the financial aspect of treatment as smooth and transparent as possible, allowing you to focus completely on your recovery.

Your Path to Recovery Knows No Borders

Navigating the path to recovery is a journey of courage, and financing that journey should not be an insurmountable obstacle. The key takeaways are clear: thanks to federal parity laws, your health insurance is required to cover addiction treatment equitably. If you have a PPO plan, your out-of-network benefits can be a powerful tool to unlock access to high-quality international care. The process, while detailed, is straightforward: verify your benefits, secure pre-authorization, and use a superbill for reimbursement.

Don’t let borders limit your options for finding the best possible environment for your healing. By understanding your insurance and partnering with an experienced international center, you can make a choice that is not only best for your recovery but also financially sound. A world of healing is more accessible than you might think.

If you’re ready to explore how your insurance can help you access world-class care in a healing environment, contact our confidential admissions team today. We’re here to help you understand your options and take the next step on your journey to recovery.